This is the handbook I would have given myself 10 years ago – when I started my journey towards financial independence. Expect a very condensed and hands-on handbook with 8 simple levels:

It is still work in progress, my aim is to cover 1 level per month starting May 2022.

Last month I stumbled on the bursting of the 2nd dot-com bubble, a historical perspective of the fiat system & bitcoin and started working on my personal FIRE-handbook:

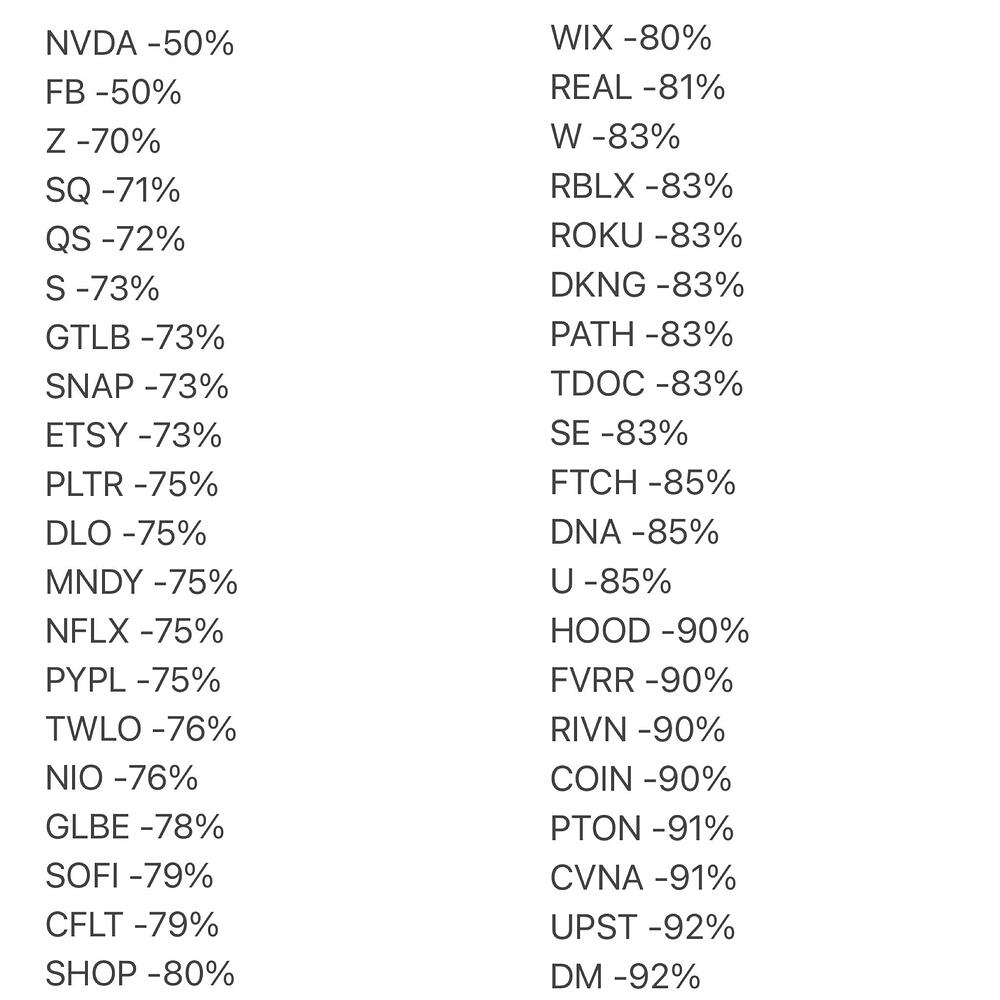

Did the 2nd dot-com bubble burst?

In my opinion, Yes. Look at the crazy corrections:

So what? Time to buy the dip?

I decided to stop buying single stocks, after my decisions within my gambling-portfolio (where I picked single stocks) did diminish my wealth faster than the Venezuelan government.

Furthermore I am fully aware of my anchoring bias, that helps me resist to jump on these “opportunities”

I am sticking to my very simple crash-action plan, which I already used during the corona crash 2020 and shifted 10% of my non-stock assets to stocks after the 20% dip.

The problem of the fiat-system and why ethereum is the mother of all shitcoins

Saifedean Ammous went on the Lex Fridman podcast to make bold statements and shared interesting historical facts about:

the success story of gold

financing of wars

printing money

why he thinks most altcoins are shitcoins

why bitcoin is a harder currency than gold

I don’t agree with everything he said but liked the discussion a lot and invite you to listen to it.

My personal FIRE Template

I promised on the Alan Frei podcast to share my personal FIRE template – realising later that without a handy checklist its absolutely useless.

So I decided to create a very condensed FIRE-Handbook with 8 simple levels:

Basic Level 0: Know where you are Level 1: Install a system to manage your money

Optimising Level 2: Reduce your expenses Level 3: Increase your income Level 4: Save & Get rid of debt

Leverage Level 5: Invest to earn money while you sleep Level 6: Use your money to improve your life

Liberate Level 7: Be financially free Level 8: Be mentally free from money

yearly yield (I only use 4% which is considered on the safer side if the money in invested in a world portfolio)

2. Use google spreadsheets and use the trend-option in graphs. It will adapt after every new entry and show you very nicely where you should land. It is preconfigured in my personal FIRE template you can use for free:

You want more posts like this?

Enter your email below to get smashed when a new post comes out .

The FIRE number is the net worth you need to have so that it (once invested) will support your expenses (until you die).

That means, once you reached that amount, you are financially free.

Here’s how you can calculate it

Yearly expenses * 25 = YOUR FIRE NUMBER

Example: Let’s assume your expenses are 50’000 per year = you will need 1’250’000 to be financially free. That means your FIRE number is 1’250’000.

Whats behind the multiplication with 25?

This simple function is based on the assumption, that you can safely take out 4% of your portfolio per year -> 100 / 25 = 4. And that again requires you to invest mostly in stocks, which did perform so good in the past 30+ years so that a take rate of 4% is considered “safe”.

Most people in the FIRE community follow this assumption since it has been widely stated and challenged with simulations. Even Vanguard wrote a paper on it I highly recommend you to read: Fuel for the F.I.R.E.: Updating the 4% rule for early retirees

Needles to say, this is just theoretical and includes some risks. Therefore most FIRE-people don’t retire the day they hit this number. Adding some buffer for unexpected expenses or a market crash in the early years of your retirement might let you sleep better at night.

What if you don’t have most of your net worth invested in stocks?

Then you simply have to define your own safe withdrawal rate which has to count in:

Your expenses

The expected yield of your portfolio

The volatility of your portfolio

Your life expectancy

Now you need to smash this into a spreadsheet and play around. Historic values might help you define what will work for you.

Are you interessted in FIRE and achieving financial freedom?

The savings rate is the share of your income after you deducted all expenses:

Expenses = 6’000

Income = 10’000

Savings = 4’000

Savings rate = 40%

What is the savings rate for?

The savings rate is one of the most important performance indicator for financial freedom, its tells you if you are moving towards financial independence and if yes, how fast:

Savings rate

Effekt

time until financial freedom*

negative

you are moving away from financial freedom

will not happen

0%

you are not moving towards financial freedom

will not happen

10%

you are barely moving towards financial freedom

40 to 75 years

20%

you are barely moving towards financial freedom

30 to 40 years

30%

you are moving towards financial freedom but you will need some patience

23 to 30 years

40%

you are moving towards financial freedom but you will need some patience

18 to 23 years

50%

you are moving towards financial freedom but you will need some patience

14 to 17 years

60%

you are moving towards financial freedom but you will need some patience

11 to 12 years

70%

you are moving towards financial freedom quite fast

8 to 9 years

80%

you are moving towards financial freedom very fast

5 to 6 years

90%

you are moving towards financial freedom at the speed of light

2 to 3 years

*the time until financial freedom is based on the hypothesis that your savings yield with 4% to 7% and that you are retired when you can retire with 4% of your total assets.

You want more posts like this?

Enter your email below to get smashed when a new post comes out .

Emotions are the reason why many investors buy high and sell low. In order to avoid that I try to detach my emotions from investing.

The market is crashing in average every 12 years, so I should experience 7 crashes in my life and thought that having an action plan would be the way to go.

How do I know if there is a crash?

I have installed the mobile app called Stock Alarm (they let you setup 5 alarms for free) and set up 5 alarms. To keep it simple I take the all time high of VT as the starting-point which is 109 USD (5. November 2021) and defined the alarms like this:

20% drawdown = 87.2 USD

30% drawdown = 76.3 USD

40% drawdown = 65.4 USD

50% drawdown = 54.5 USD

60% drawdown = 43.6 USD

Every time an alarm is triggered, I get a push notification and an e-mail.

The actions during the crash

After every alarm (same day) I shift the following amounts of non-stock assets to stocks:

20% drawdown = 10% of non-stock assets

30% drawdown = 15% of non-stock assets

40% drawdown = 20% of non-stock assets

50% drawdown = 25% of non-stock assets

60% drawdown = 30% of non-stock assets

My target allocation looks like this:

80% Stocks

5% Bonds

5% Commodities

5% Real estate

5% Cash

Which means that I will reduce the other asset classes and eventually end at 100% stocks after the 5th alarm.

The actions after the crash

As soon as a new all-time high is more or less reached (-10%), I sell the stocks to rebalance back to my target allocation (only if needed since I invest every month, no rebalancing might be needed).

Log-book

What happened so far?

12. May 2022 | 16:03 I got the following alarm: “The price of Vanguard Group, Inc. – Vanguard Total World Stock ETF is below the $87.20 limit. The current price is $87.12 ( -$0.95, -1.07%). Notes: Ship 10%”

So I rebalanced accordingly and since my cash position was over 5% I simply just bought the stocks the same day for 10% of the value of my non-stock assets.

14. February to 20. March 2022 The global stock market crashed due to the pandemic. I hadn’t set up the alarms back then but made the same calculations on a note in my smartphone and bought 2x for 10% during the drawdown.

You want more posts like this?

Enter your email below to get smashed when a new post comes out .

The main purpose of my FIRE Template is to achieve the goal of financial freedom. This template tells me where I am now, how for am I away from financial freedom and am I moving towards or away from it.

How to use it?

Click here to access it and make a copy. I suggest you use Google Spreadsheets as well, so that you can use the graphs I created.

1. Decide how often do you want to update it. I personally do it monthly but quarterly, half-yearly or yearly will work as well. Adapt the row “date” to the schedule you want. Go as back in the past as you have the data available.

Let’s look at the definition of an asset. The definition from Wikipedia is “…an asset is any resource owned or controlled by a business or an economic entity.”

This means that everything you as a private person own and is valuable to somebody else is an asset. But not every asset is relevant for financial freedom, so I focus only on assets which already generatecashflow or can be traded easily with something who does generate cashflow, like:

Savings in bank accounts

ETFs, Shares & Bonds in (depots / brokerage accounts)

Savings in pension funds

Savings in retirement accounts (3rd pillar in CH)

Cash

Cryptos

Precious metals (gold, silver, palladium, etc.)

Loans you gave out

Privately held companies

Real estate you rent out

etc.

I tend not to focus on assets which are not generating cashflow, do decrease fast in value or are hard to trade:

Cars

Jewellery

Watches

Art

Rent deposit

Shares from early stage start-ups

Real estate you own and live in*

etc.

*This is actually somehow disputable. On one hand, if you own and live in your house it’s not generating cashflow and can not be sold/traded easily because you are living there. On the other hand you could argue that you could move out, sell it and go rent a place at any time. So feel free to do whatever you think is right.

Value of each asset

Every asset which is traded publicly has a actual price based on the last trade, so the value of these assets can be looked up.

For everything else I would take a price you are 100% sure to get for the asset and be rather on the safe side. I don’t try to polish the sum of my assets, since it will be used for calculations I would like to trust.

How to summarise and monitor my assets?

I use a simple spreadsheet where I update the value of my assets over time. You can create your own spreadsheet or use my personal FIRE template.

You want more posts like this?

Enter your email below to get smashed when a new post comes out .

Most people I talked with about optimising their finances, didn’t know where they actually stand. Do you? If yes, you should be able to answer these questions precisely:

My assets are: ____________

My debt is: ____________

My income is: ____________

My expenses are: ____________

Based on these 4 numbers, you can state:

My net-worth is: ____________

My savings-rate is: ___ %

My FIRE number is: ____________

I will be financially free on the: DD/MM/YYYY

My net-worth in 10 years is projected at : ____________

If you have this numbers ready, you are a badass. If not, you can use my personal FIRE template and/or follow these steps:

Great, now you have the data ready to calculate some performance indicators. If you use my personal FIRE template, it will do it for you. Otherwise you have the steps here:

Now you have the overview and can ask yourself the following questions:

What are my dreams I can buy with money? Write down what and how much it will cost (early retirement (1’500’000), Tesla Model Y (60’000) / house (500’000) / watch (8’000) / etc.)

Is the projection of my net-worth in 10 years in-line with the dreams?: Yes / No Which dreams are possible? which aren’t?

Looking at my financial situation and the future achievement of my dreams, I feel: euphoric / happy / neutral / insecure / stressed / anxious? Write down the answer and why

You might wonder, what is this all about? Aren’t you here to get rich quick? You expected 10 hacks on how to half your expenses. Don’t worry there are more hacks than you need. The key element to financial optimisation is to know where you are today and where you want to go. That means, you need to know what you are optimising for!

If you like the situation you are in now, the projections of your net-worth is aligned with your dreams and you are euphoric or happy about your financial situation: Your financial management is good enough. Leave this blogpost instantly and focus on other things. You will waste your time.

If that is not the case, welcome to the club. Take the time to calculate your starting point and answer the questions above to have a first idea what you want to achieve. This will guide you in the next levels.

You want more posts like this?

Enter your email below to get smashed when a new post comes out .

Defining income sounds easy, but it actually isn’t. Even wikipedia has a hard time to define it, since the meaning differs from the perspective (law, economics, etc.).

To keep it simple you can add up every income source you have, like:

Salaries

Pension plan contributions

Dividends

Rents from stuff or real estate rented out

Royalties

Profits from owned businesses

etc.

How to define the amount per Income source?

I take the value which is available to me, directly or indirectly. So if taxes or deductions are made which are not available to me, like unemployment insurance, I don’t count them in my income. To make it easy, use the amount which is credited in your bank account.

Be aware that it is relevant to know the “real” income of each source. The “real” income is what is left in your bank account after deducting every expense which is directly linked to the income source (which has not yet been paid when the income arrives in your bank account).

If your work contract states a salary of CHF 5’000 and you have direct deductions of CHF 500, CHF 1’000 income taxes and you need a car which costs CHF 500. You wouldn’t have these expenses without that job. If thats the case your real income is CHF 3’000.

Knowing the “real” income of each source will help you evaluate the value for you of each source. So don’t forget to add all expenses linked to the income sources as expenses and label them accordingly.

How to summarise and monitor my income?

I use a simple spreadsheet where I update the value of my income over time. You can create your own spreadsheet or use my personal FIRE template.

You want more posts like this?

Enter your email below to get smashed when a new post comes out .

Leave a Reply